FCA File Checking: What Should Be Reviewed in an Advice File?

The FCA are notoriously vague on details when it comes to what “perfect” looks like to them. You see the problem for a regulator is that while they set the standards. As soon as they offer up a perfect mannequin, hey-presto, every case is a copy mannequin. They do not like to lead, or be didactic in their requirement. Once I lived in a picturesque listed terraced cottage in the Cotswolds. They did not like the colour of our door, so an enforcement letter asked me to change it to match the other doors. Of course every other door was white, and they got me to paint my door white – without ever saying the word, “white”. An amusing exchange of letters, sits in my archives. It is in the nature of regulation – cajole and persuade, in the negative and guide with a stick. Of course this makes our job as IFAs where our advice service is regulated, just so much harder.

Suitable, unsuitable and unclear: how FCA assessments have changed

There have been two strands emerging from this. Firstly firms who have been under the microscope of the FCA have developed an approximate template for themselves. These of course do not match exactly, but in general they rhyme, and if you follow their templates, the files roughly fall into three categories, of suitable, unsuitable and unclear.

These three categories have been in common useage since the 2006 Pension review on switching, and were used in the 2016 FCA Post RDR Industry Review. The FCA reviewed 1,142 advice files from 656 firms and assessed them against the Conduct of Business Sourcebook (COBS). They published their findings, FCA Assessing Suitability Review but it is not exactly an easy read, and many commentators at the time were astonished to find that FCA claimed 93% suitable advice, when in fact 42% of the files were also deemed deficient of information or material in one way or another (usually classified generally in the compliance industry as “unclear”). Of course they allowed most of those 42% of files that missed some key documents to pass as presumed suitable, since disclosure is only a part of suitability, and not suitability itself. Still with me? Checking other people’s files and drawing conclusions from what is a record of a conversation, is not the easiest activity, and it gets worse!

The FCA Investment Advice Assessment Tool

The three advice outcomes of Suitable, unsuitable and unclear did not make it into the filechecking template or commentary for the next round of FCA thinking. In 2025 The FCA issued further file checking guidance. This is embedded in a document called the FCA Investment Advice Assessment Tool (IAAT) and is located here

FCA Investment Advice Assessment Tool (IAAT)

It is at pains to avoid calling itself a suitability checker, rather the FCA describe it this way:

“The template does not make an automatic decision on the suitability of the investment advice; it is there to support you.”

The term UNCLEAR IS actually abolished. In fact, the document seems to make mincemeat of its own 2016 review. In that last review (the only industry wide review ever conducted) they found 42% of files lacking information. But in 2025 the FCA say:

“You cannot assess advice as suitable if there is a Material Information Gap. In this case, you can only conclude that advice is unsuitable.”

So if you used this 2025 template against the 2016 RDR review findings, then you are left with a very uncomfortable number – that 49% of files were not just unclear, but actually unsuitable in 2016. Perhaps that is why the FCA scrapped the planned follow up Review.

How has your firm improved its results in that time? Do you have a benchmark from 2016 to 2025 to show to the FCA?

What should be reviewed in an advice file?

This is a slight diversion to the question of “What Should Be Reviewed in an Advice File?” but it helps sets the scene for apparently concrete lists of requirements that soon fall away under challenge into subjective judgement templates.

The requirements are embedded in COBS, the conduct of business sourcebook. These are the rules, as far as they are written down. Seasoned commentators will show you that the FCA keys lie in principles, and that the 12 principles for business effectively act as the benchmark of what goes, and what doesn’t go. Back to 2016 and the FCA published a list of requirements under the following headings,

Know your client KYC (known as fact finding to industry)

Research and due diligence

Recommendations

CIPs / replacements / insistent clients.

FCA guidance on assessing suitability

It looks by comparison today in the post consumer duty era to be a somewhat vague statement of requirements, and has been overtaken by industry who use much higher standard and more detailed assessment of files and suitability reports.

How Consumer Duty has changed file checking

Rather than simply following processes and demonstrating procedural compliance, firms must now actively deliver good outcomes for retail customers, or rather in the way that compliance adds a further dimension to any activity, we must now SHOW how we have actively delivered good outcomes.

Consumer Duty is intended to become embedded within your day-to-day operations - and we must show this on request.

For advice firms this means being able to evidence in the advice files:

Suitability of the advice

Fair value for the customer

Customer understands what they have bought

Customer support that will follow

Consistency in firm or adviser behaviour

Fair treatment for customers who show signs of vulnerability.

Ongoing service delivery post sale

Continual monitoring and improvement

You can no longer assume good outcomes are embedded, in the old days this was by measuring the lack of complaints, or some survey or other conducted on your clients, or the feedback file, full of loving letters from happy customers. You've now got to get on the front foot and be able to prove what you are doing. Networks and Nationals have changed and are far more proactive today.

In a stroke, file-checks has become one of the most important Consumer Duty controls available to firms.

The FCA's own advice assessment and disclosure review templates provide a strong indication of the regulator's expectations, but it is never easy for the regulator even when it wants to get didactic. For a variety of reasons that I never have fully understood, they simply will never tell you what exactly to do, or how to do it, even informally in private chat, stepping back and saying when challenged, “how you do that is for you to decide...”

Notably in all the documents and papers reviewed for this article, the FCA never once mention the one word that is probably used more than any other word in an IFA or mortgage broker’s office: FACTFIND!

The word factfind is not mentioned once in the extensive FCA rulebook. They call it “information gathering” today, and previously called it KYC, or know your client.

The closest that we get to the FCA telling us exactly what they want is in this text:

"We are publishing the IAAT to help firms understand the methodology we use in our file reviews of investment advice"

FCA Investment Advice Assessment Tool (IAAT) But even this text is covered in copyright protections, and it can only be used by the industry under a licencing agreement, which means restricted access, and only where "any reproductions of the IAAT will be marked with a notice in the following terms:© Copyright FCA 2024"

It is almost as awkward as those HM Customs copyright protections on passport photocopies, observed only in the breach!

The FCA’s information-gathering questions

There is a whole raft listed of closed end yes/no questions for file checkers to use when reviewing a file.

Has the firm obtained the essential facts about the client?

Has the firm obtained the necessary information regarding the client's objectives?

Has the firm obtained the necessary information regarding the client's investment risk profile?

Has the firm obtained the necessary information regarding the client's knowledge & experience?

Has the firm obtained the necessary information regarding the client's expenditure and any planned changes?

Has the firm obtained the necessary information regarding the client's financial situation?

Has the firm obtained the necessary information regarding the existing product(s)?

Has the firm obtained the necessary information regarding the proposed scheme(s) or investments(s)?

It’s a blunt tick box exercise, and it develops, asking the checker to provide a

Tool rating on whether firm has obtained necessary information

Assessor's rating on whether firm has obtained necessary information

Assessor's rationale/evidence for information collection rating (include reference to specific rule breaches).

Despite the file being "not compliant", do you consider it poses a high or low risk of a poor outcome?

QA rating on whether firm has obtained necessary information

QA summary of changes made and feedback to the file assessor

QA suitability rating

REASONS WHY the FILES FAIL, according to 2025 paper

FCA Investment Advice Assessment Tool (IAAT)

The key reasons for failure may give you key clues as to what to checkers should review, and I summarize these below:

Disclosure failures - ie the mandatory items such as IDD, cost disclosure, restricted/independent confusion.

Timescales (eg to retirement or specific planned event)

Switching for no purpose

Replacement for no benefit

Costs and fees

Tax

Risk mismatch

Capacity for loss mismatch

Lack of explanation on ongoing requirements

The three principal areas assessed by the FCA

This all feeds into THREE key boxes for the results summary:

Information collection

Disclosure

Suitability

It sort of works, but somehow the document is only a guide, and, as they say themselves, should not be used as the key checker document. So we are back to designing our own.

What information must advisers collect under COBS 9?

The real source for an answer of what should be reviewed in an Advice File lies in COBS9, and more particularly in the industry interpretation of the same. COBS 9 – Suitability Requirements is the core FCA Handbook section governing advice suitability.

The suitability rules require advisers to gather up a fact find including all the following:

Client objectives

Financial situation

Knowledge and experience

Ability to bear losses

Risk tolerance.

so a lot of yes no questions to be answered about the file. Has the adviser

Collected sufficient client information.

Understood the client's circumstances.

Matched recommendations to client needs.

Justified the recommendation.

What should appear in a suitability report?

Then there is another section COBS 9.4 – Suitability Reports. This section can be useful because it sets out what must appear in a suitability report. The FCA states that a suitability report must:

Specify the client's demands and needs.

Explain why the recommendation is suitable.

Explain any disadvantages.

Provide personalised reasoning.

A file checker should review whether the suitability report contains:

Client objectives

Risk profile

Capacity for loss

Recommendation rationale

Costs and charges

Alternative options considered

Demonstrates:

Clear adviser reasoning

Client-centred recommendations

Balanced explanation of risks and benefits.

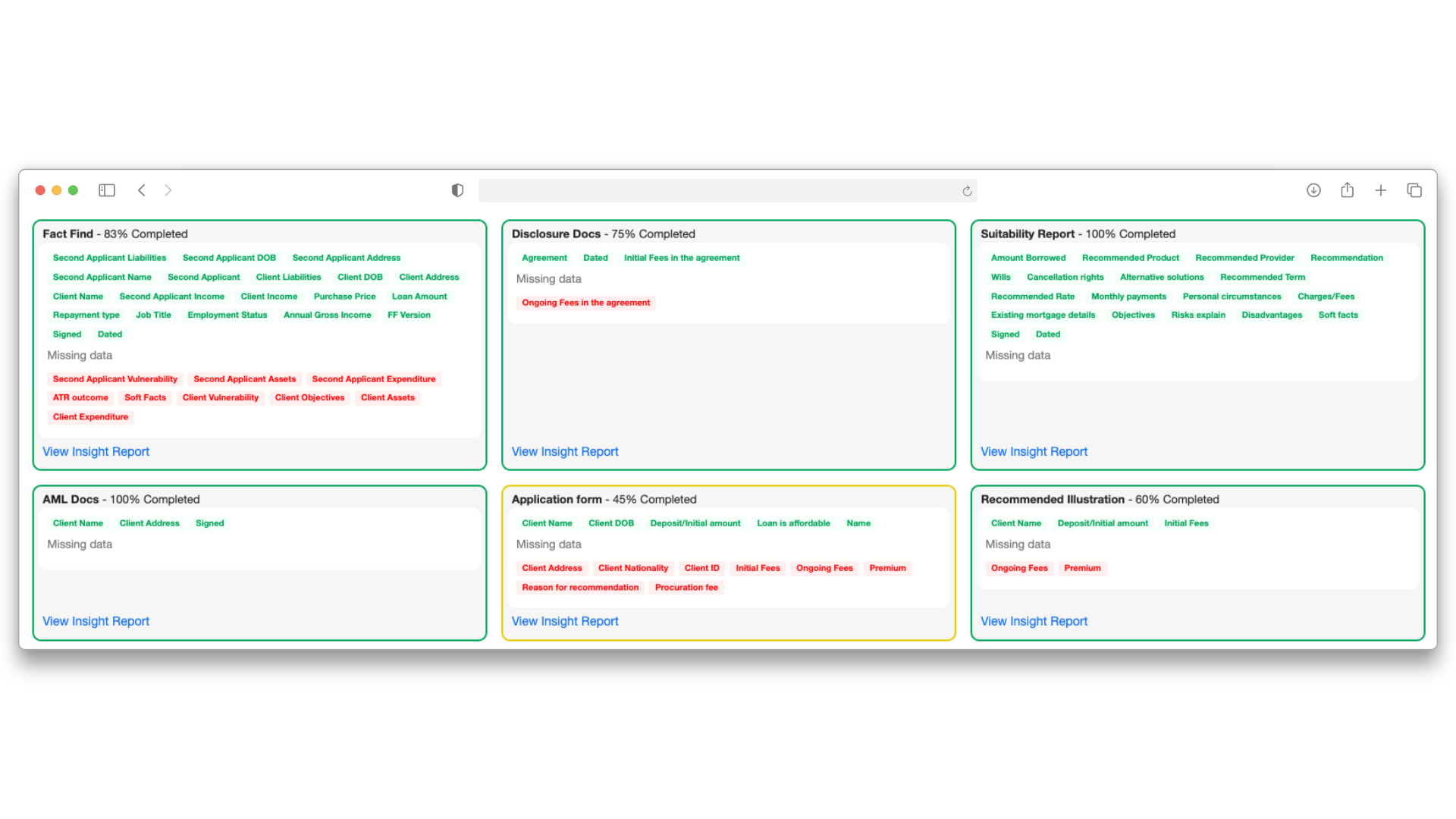

So much for FCA who are the final arbiter, but file checkers know there is more to do and say on a file. Our compliance partner IFAC use a detailed assessment template, and give brief feedback to advisers, both when files are suitable, and when they fail and when unclear.

What do IFAC say?

What does a good file look like? Following COBS 9.2.1

Filechechers in general follow the following headers / headings

Disclosure Documents

Anti-Money Laundering Verification

Data Protection

Know Your Client

Attitude to Risk

Research

Illustration

Suitability Report/Letter

Additional Considerations

Any missing items are immediately identified, and this forms the basis of what is going to be checked for actual suitability. If the item is missing, then frankly there is no point proceeding and checking the suitability of the file. BAT call this the COMPLETENESS check.

The BAT advice-file checklist

In more detail the BAT AI filechecker system looks quickly for

Client Agreement

Copy on file

Dated prior to advice

All details correct

AML

Has the client’s identity been checked?

All details correct

Disclosure

Data Protection

Privacy Notice on file

And then it strips out the FACT FIND FF into hard and soft facts.

FF Hard Facts

Personal Information

Are there sufficient details surrounding the client's personal information to allow a recommendation to be made?

Financial Information…

Are there sufficient details surrounding the client's financial information to allow a recommendation to be made?

Does the factfind FF contain sufficient information on Income and Expenditure (current and future where applicable), Assets, Liabilities?

FF Soft Facts

Are there sufficient soft facts/discussion notes on file to support the advice?

Help support the recommendation

Key drivers for advice

What does it mean to the client?

Future aspirations/plans – any changes coming that may need to be considered when choosing product

Vulnerable Client

Checked, documented and provisions put in place

Product/Feature Requirements

If particular product or feature required, is this detailed and properly recorded?

Is the FF Uptodate with correct client details?

Nature of relationship between parties entering agreement

Dated prior to advice

Sufficient level of detail of income and sources of income

Source of Funds clear

E.g. Details of other plans, cash holdings

Sufficient level of detail of expenditure

Ideally broken down, or if not broken down, sufficient notes to ensure clear FF, that means

Affordability established, both

Immediate and ongoing

And as for the Planned Retirement Age

Does the recommended plan meet the need?

Assets and Liabilities

Does anything need repaying?

And we come to

Knowledge and Experience

FF Needs and Objectives

And

SMART

Specific

Measurable

Achievable

Realistic

Time Bound

BAT AI filechecker looks at

Discussion Notes to ensure that Reasons Why can relate back

RISK

Risk Profiling

Risk Profilers

Capacity For Loss

Knowledge and Experience

Discussion Notes

Risk the client is willing to accept

Amendments to profiler outcomes

CFL

Volatility

Attitude to Risk

Has the client's ATR been sufficiently established?

Has there been a documented conversation of the outcome and agreed ATR?

Have any conflicting or non-committal answers been challenged?

Capacity For Loss

Has the client's CFL been sufficiently established?

Knowledge and Experience

Has the client's Knowledge and Experience been taken into account in establishing the client's ATR?

Existing Plans

Is there documentation on file detailing full ceding scheme information?

Generic

Product Features

Client specific

Costs and Charges

Underlying funds

Mapped to ATR?

Performance

Tax - CGT, IHT, Pensions etc

New Plans

Is there research on file to prove why the provider has been selected?

Is this confirmed in the SR?

Software use

Proof of why selecting a provider and plan

Cashflow

Forecasting future finances

Whether a client is on track to meet their goals

Recommendation helps ascertain why a client shouldn’t take a course of action

Updated regularly as part of review process

Scenario Planning/Stress Testing

Centralised Investment Propositions (CIP)

Centralised Due Diligence

Updated annually

FG12/16 – July 2012

Replacement Business and Centralised Investment Propositions

A firm must “ensure that it is not ‘shoe-horning’ clients into the CIP”

Only recommended to clients when it is suitable for those clients

Flowchart? Decision Tree? Matrix?

CIP

Dated and discussed with client prior to application

Consistent with recommendation and all details correct

Product

Provider

Client

Monthly cost

Investment Amount

Product Terms

Additional Features

Costs and Charges

SR

Introduction

Has adviser confirmed their status, fee agreement (if appropriate) & basis on which advice is to be given?

Have any other needs been identified that are not to be addressed now sufficiently documented and deferred to a future date?

Consistent with rest of file and details correct

Client Objectives

Illustration

Factfind information

Attitude to Risk

Adviser Name and Firm Details

SR

Client details and Personal Circumstances

In Suitability Report

Referral to Factfind and copy provided

Appropriate

Vulnerable Client

Knowledge and Experience

SR

Recommendation

Clear and detailed

Product Features

Features explained sufficiently

Is the recommendation suitable?

Does the recommendation meet the client's needs and objectives?

Is the recommendation in line with the client's ATR?

SR Reasons Why

Provider

Match in with the research on file

Has the provider selected been effectively justified and suitable reasons provided on the report?

Are there sufficient reasons why provided for the Product, Provider, Platform, Investment, Income etc?

Do they relate back to the client’s Needs and Objectives?

SR

Alternative Solutions

Alternative Products

Alternative Sources

Reasons why discounted

Client specific

Advice based

Any recommendation MUST be driven by the adviser based on what they believe to be the most suitable advice for the client, rather than simply facilitating a desire

Disadvantages and Risks

Disadvantage – what WILL happen

Risk – what MIGHT happen

Appropriate to the product type and specific features recommended

Confirmation KFD and Illustration enclosed

Cooling Off Notice/Change of Mind

Clear statement

Remuneration

Has Adviser Remuneration disclosure been provided in hard format in the SR?

Relevant Product Costs & Charges disclosure

TCF/Consumer Duty/Prevention of Client Harm

Suitability

Fair treatment

Fair value – does the cost and benefit balance

Clear, Fair and not misleading

Taking into account client characteristics

FILE CHECK COVERS....

Suitability

Disclosure

Initial Client Disclosure and Agreements

Costs and Charges

MiFID II requirements

Anti Money Laundering

File Excellence

FILE CHECK ERRORS:

Investment

Know Your Client

Risk Profiling

Inconsistent

Lack of Discussion Notes

Lack of Soft Facts/Discussion Notes

Alternative Products

Alternative options not sufficiently discounted

Pension

Know Your Client

Risk Profiling

Inconsistent

Lack of Discussion Notes

Lack of Soft Facts/Discussion Notes

Lack of State Pension information when nearing retirement/pension income planning

Inconsistencies within FF or between FF and SR

Needs & Objectives

Unclear/Inconsistencies from FF to SR

Not SMART

Recommendation and Suitability

Reasons why not relating back to objectives

Alternative Solutions not discounted

Why advice file checking is complex

If like most IFAs and brokers, you are astonished at the amount of information that is checked by compliance and needs confirmation and checking, and maybe have speed-read the above requirements, then you will reach the same conclusion. It is complex and subjective, it takes time and energy to check files.

How Consumer Duty raises the standard

The key for BAT is the Consumer Duty that is sweeping change and increases the amounts at stake… also known as “upping the ante” the standards have risen for advisers, and a chill wind awaits those who haven’t changed. Due diligence audits are standard fayre now for firms selling up, joining other organisations or seeking to grow. Expect in these cases to see all your files put through a BAT auto file check review using AI to extract key trends.

Why traditional file sampling is no longer sufficient

The FCA's New Direction Means file checking is no longer about sampling perhaps 1% or 20% of files. Although the FCA has committed to becoming a "smarter regulator" and reducing unnecessary regulatory burdens, it has simultaneously reinforced that Consumer Duty sits at the heart of how firms deliver good customer outcomes, and that means more checks, and more requirement for evidence, outcomes monitoring consistency. It takes the filechecker some two hours to work through a full file check, so the economics increasingly point to using AI for file checking.

Firms must be able to demonstrate ongoing Consumer Duty compliance across all advisers, all advice types and all customer segments. So how to do this when only sampling files for checking?

This shift will fundamentally change the oversight over the next five years, and introduce a higher standard of care for regulated firms.

A firm reviewing only 10% of advice files cannot confidently conclude that the remaining 90% to 95% delivered good customer outcomes. The larger the adviser population, the greater this risk becomes. With only 50 advisers, a firm can expect two cases per week per adviser, so that will rapidly increase to

5,000 advice files per year

And with a 10% sample they would previously review only 500 files, and leave 4,500 cases untested. This cannot continue.

While the FCA has not explicitly mandated 100% file reviews, the direction of travel is becoming increasingly clear, and pre-sale filechecking means taking risk off the table.

Consistent Oversight

Every customer interaction receives scrutiny.

Adviser Benchmarking

Patterns emerge across adviser populations.

Early Risk Detection

Pre-empt issues before they become systemic.

Improved Consumer Outcomes

Remediation at pace rapidly.

Better Management Information

Senior managers gain genuine visibility of advice quality.

Stronger Consumer Duty Evidence

Boards can demonstrate proactive monitoring.

The role of AI in advice file checking

Technology is changing this equation by making this cheap and affordable, and with that it becomes close to a necessity. AI can cope in realtime withal the following that hitherto took months to achieve…

Volume

Consistency

Speed

Trend analysis

Cross-adviser comparisons

AI-assisted review systems can help firms analyse:

Suitability report quality

Consumer Duty outcomes

Disclosure consistency

Vulnerable customer treatment

Ongoing servicing evidence

Charging transparency

Adviser behaviour patterns

Most importantly, AI-assisted review can help identify risks across entire adviser populations rather than isolated samples. It does not remove the need for human oversight, and if using the BAT system we achieve this with a simple “escalate” button to request filechecks.

Compliance professionals can therefore focus their expertise on higher-risk cases and complex judgement areas.

AI-supported review with human oversight

The future is unlikely to be AI replacing compliance reviewers, it will be AI identifying risks and humans making regulatory decisions.

Continuous quality monitoring using AI-assisted review capabilities, ultimately gives the ability to assess 100% of advice activity in order to provide compelling evidence that good customer outcomes are being delivered consistently across the business.

Sources

- FCA: Assessing Suitability Review Findings from the FCA’s review of pensions and investment advice files.

- FCA: Investment Advice Assessment Tool (IAAT) The FCA’s methodology and supporting information for investment advice file reviews.

- FCA: Assessing suitability FCA material covering know-your-client information, research, due diligence and recommendations.

- FCA Handbook: COBS 9 — Suitability The FCA Handbook chapter setting out suitability requirements.