How to Reduce Compliance Risk in Financial Advice Offices

A practical guide to stronger file checking, clearer audit trails, better management information and more consistent FCA compliance across financial advice firms to reduce compliance risk.

Reducing compliance risk is one of the biggest operational challenges facing financial adviser firms. The risk is not limited to whether advice is suitable. It also sits in how consistently advisers follow the firm’s process, how well client files are documented, how issues are escalated, how management oversight is evidenced, and how quickly compliance teams can spot patterns before they become business-wide problems.

For many adviser offices, the challenge is not a lack of compliance knowledge. It is the difficulty of applying that knowledge consistently across advisers, administrators, paraplanners, file checkers, managers and senior leadership.

The FCA’s direction of travel makes this even more important. In its 2025 financial advice firms survey , published in April 2026, the FCA said it had gathered responses from over 4,100 firms and analysed data on around 31,000 registered financial advisers. It also said this data would help it identify risks across the sector and support more data-led proactive supervision.

That means advice firms need to think carefully about how they evidence control. Good intentions are not enough. Firms need clear records, repeatable processes, robust file checking, effective management information and reliable audit trails.

What does compliance risk mean in an adviser office?

Compliance risk is the risk that a firm fails to meet regulatory expectations, internal standards or client outcome requirements. In a financial adviser office, this can arise from many areas, including:

- Incomplete fact finds

- Weak suitability rationale

- Missing or unclear client objectives

- Poor evidence of attitude to risk and capacity for loss

- Inconsistent disclosure

- Unclear advice charges

- Inadequate Consumer Duty evidence

- Weak vulnerable client identification

- Missed annual reviews

- Poor record keeping

- Inconsistent file checking

- Limited management oversight

- Lack of audit trail

In practice, compliance risk is usually not caused by one large failure. It often builds through small gaps in process, documentation and follow-up. A missing note here, an inconsistent suitability explanation there, an unresolved file check action elsewhere. Over time, these small issues can create serious risk for the firm.

The key is to identify problems early, fix them quickly and understand whether they are isolated cases or part of a wider trend.

Why FCA compliance expectations are becoming more evidence-led

The FCA’s Consumer Duty has shifted the conversation from “did the firm follow a process?” to “can the firm evidence good outcomes?” The FCA has stated that Consumer Duty remains a priority under its 2025–2030 strategy and that embedding the Duty is critical because it is relying on the Duty rather than creating more prescriptive rules.

For adviser firms, this creates a clear operational requirement: firms need to show that their compliance framework is working in practice.

The firms best placed to manage this environment are those that can connect compliance activity with evidence. This is where many traditional processes struggle.

A spreadsheet might track whether a file was checked, but it may not show the full picture: what was checked, who checked it, what issues were found, what action was taken, whether the action was completed, whether similar issues appeared elsewhere, and whether management reviewed the trend.

That is why reducing compliance risk requires more than file checking alone. It requires a joined-up control framework.

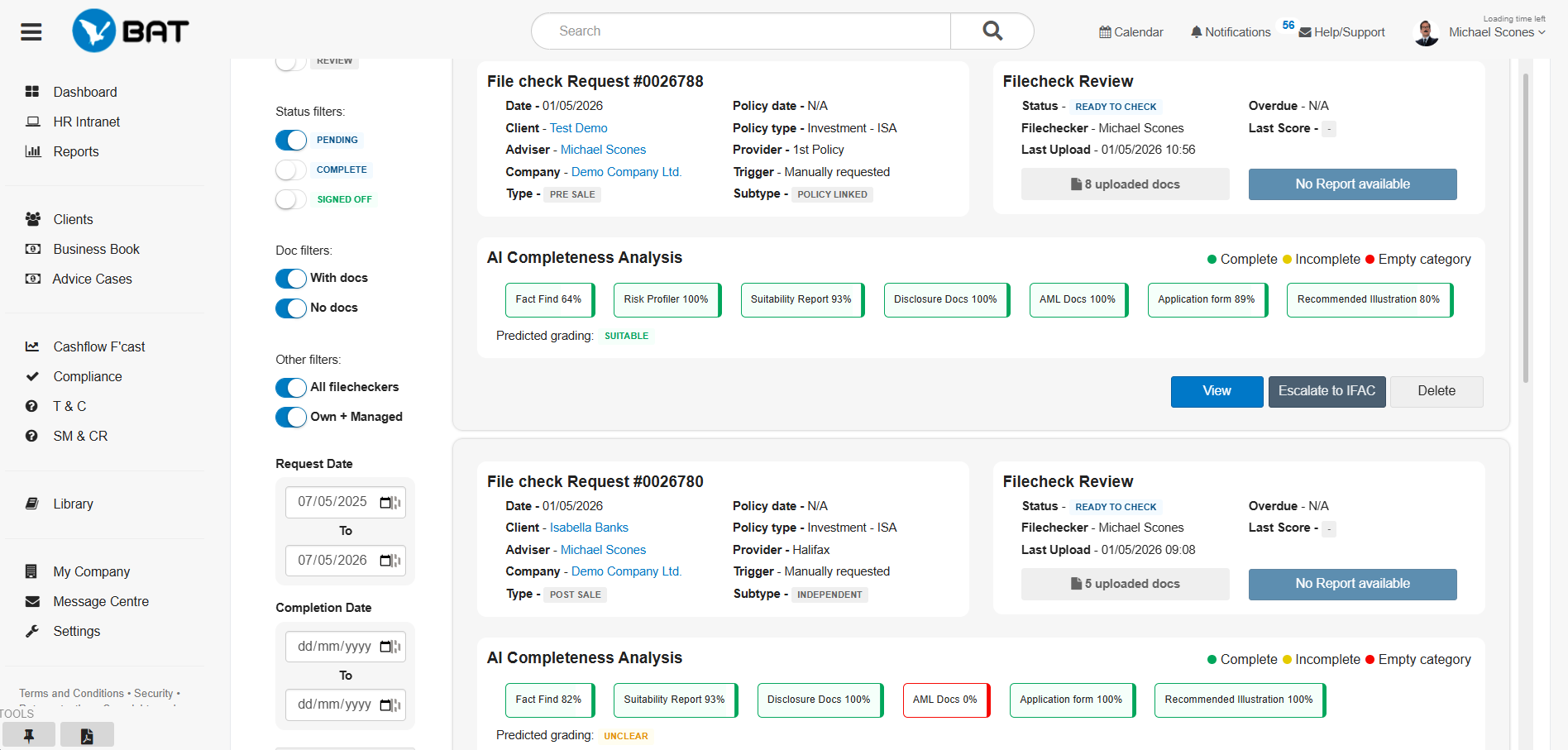

The role of file checking in reducing compliance risk

File checking remains one of the most important tools for reducing compliance risk in financial advice firms. It helps firms assess whether advice has been documented properly, whether the adviser followed the required process and whether the client file supports the recommendation made.

The FCA’s Investment Advice Assessment Tool is designed to help personal investment firms understand how the FCA assesses the suitability of investment advice and disclosures to consumers.

A strong file checking process should assess more than whether documents are present. It should consider whether the file tells a clear and complete story.

A file should answer questions such as:

- What did the client want to achieve?

- Was the client’s current position understood?

- Were objectives clearly recorded?

- Were risks explained in a way the client could understand?

- Was the recommendation suitable?

- Was the advice charge clear?

- Were alternatives considered?

- Was vulnerability considered?

- Were conflicts or limitations disclosed?

- Is the rationale strong enough for a third party to understand?

Common compliance risks in adviser offices

1. Inconsistent advice processes

One adviser may document objectives in detail, while another records only a short summary. One team may follow a pre-sale checking process, while another relies mainly on post-sale review. One office may use updated templates, while another continues using older versions.

This inconsistency creates risk because the firm cannot easily prove that standards are being applied across the business.

2. Over-reliance on spreadsheets

Spreadsheets are common in compliance teams because they are flexible and familiar. However, they were not designed to manage complex compliance operations across growing firms.

- Version control problems

- Limited audit trail

- Duplicated data entry

- Lack of live visibility

- Manual reporting

- Inconsistent formatting

- Difficulty tracking actions

- Poor scalability

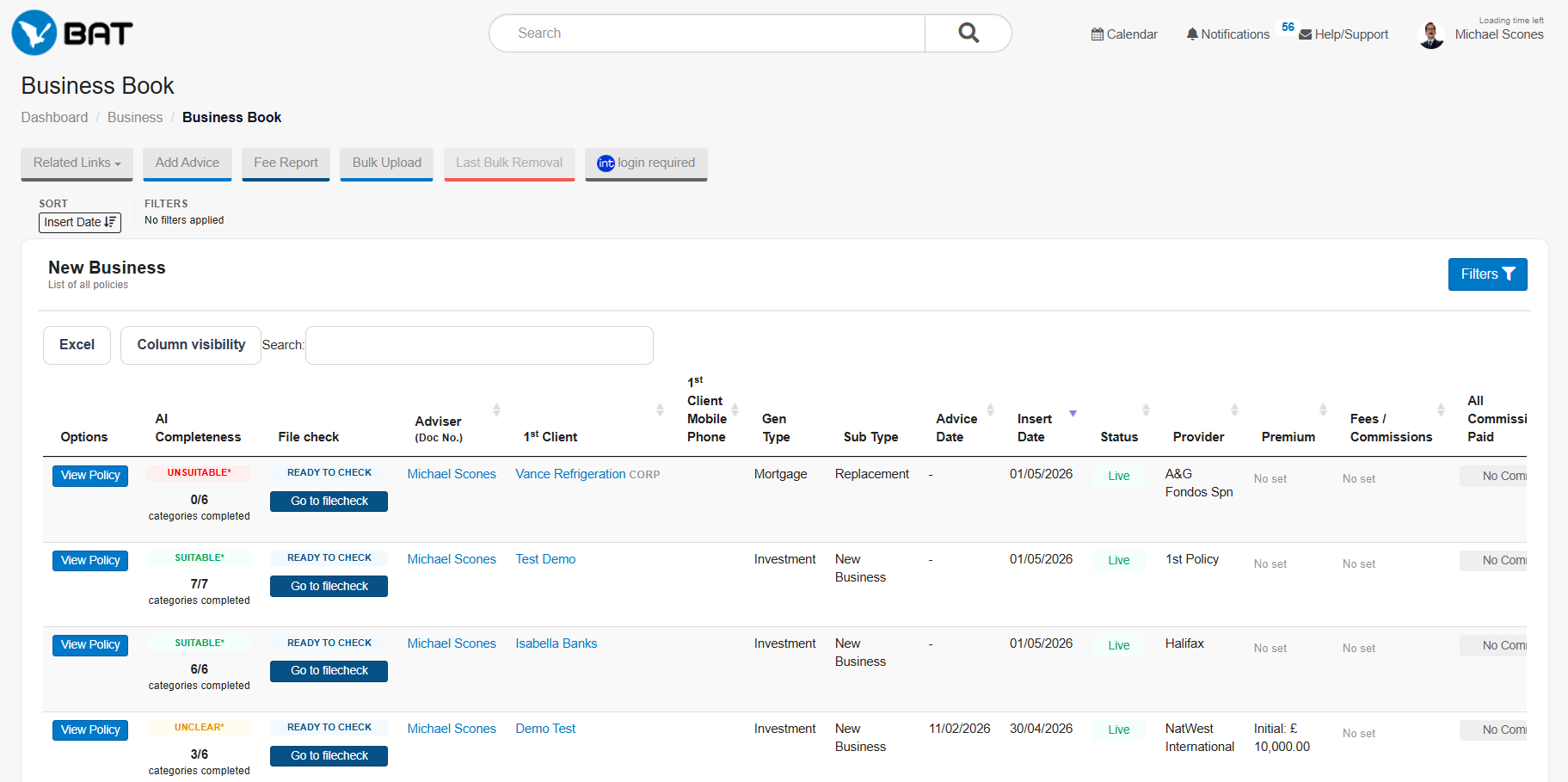

Replacing fragmented spreadsheets with a centralised system can reduce risk by giving compliance teams one place to manage reviews, actions, outcomes and reporting. BAT’s compliance software for financial advisers is designed to help advice firms centralise compliance operations and improve oversight.

3. Weak audit trails

A weak audit trail makes it difficult to answer basic questions:

- Who reviewed the file?

- What was the review outcome?

- What issues were found?

- Who was responsible for fixing them?

- When were actions completed?

- Was the case rechecked?

- Was the issue escalated?

- Was management informed?

4. Reactive rather than proactive compliance

Many firms only identify compliance issues after the advice has been given or after a file has already reached the compliance team. This creates avoidable rework and delays.

A better approach is to build compliance checks into the workflow earlier. That could include pre-submission checks, missing information alerts, required field validation, template controls and AI-assisted prompts that highlight gaps before the file progresses.

5. Poor visibility for managers and senior leadership

Senior managers need confidence that the firm’s controls are working. They need to know where risk is increasing, whether remedial actions are completed, whether adviser performance is improving and whether Consumer Duty outcomes can be evidenced.

How to reduce compliance risk in practice

Step 1: Map your highest-risk advice areas

Not every case carries the same level of risk. Firms should identify the advice types, advisers, client segments and processes that require closer monitoring.

- Pension transfer or retirement income advice

- Complex investment recommendations

- Vulnerable clients

- High charges

- Replacement business

- New advisers

- Complaints-linked themes

- Files with missing information

- Cases involving unusual objectives

Step 2: Standardise your file checking framework

A file checking framework should define what is checked, when it is checked, who checks it, how it is graded, what counts as a material issue, how feedback is recorded, how remedial action is tracked, when escalation is required and how trends are reported.

The market already recognises the importance of structured file checking. Verve describes file checks across suitability, disclosure and process. Paradigm’s file review service includes pre-sale, post-sale, regular and ad-hoc file reviews. Ruleguard positions client file reviews around assessment and grading against FCA principles.

Step 3: Move from sample checking to smarter coverage

Traditional file checking often relies on sampling. Sampling can still have a place, but it may miss important issues if the sample is too small or not risk-based.

- Checking higher-risk cases automatically

- Reviewing all cases from new advisers

- Applying thematic checks across specific advice types

- Using AI-assisted tools to highlight missing information

- Escalating only the files that need human review

- Using data to identify adviser or office-level trends

For example, Aveni positions AI oversight around scaling file checking and supporting broader monitoring across advice networks.

Step 4: Build compliance into the adviser workflow

Compliance should not feel like an obstacle at the end of the advice process. It should be embedded into the way advisers work.

- Structured case workflows

- Required fields

- Standardised templates

- Automated reminders

- Document checklists

- File completeness checks

- Action tracking

- Real-time file review status

- Manager visibility

Step 5: Track remedial actions properly

Identifying an issue is only half the job. The firm must also show that the issue was addressed.

- The issue identified

- The risk rating

- The owner

- The deadline

- The action required

- Completion status

- Evidence of completion

- Recheck outcome

- Escalation notes, where relevant

Step 6: Use management information to spot trends

Compliance MI should help firms answer practical questions:

- Which advisers have the highest number of file check fails?

- Which advice types create the most issues?

- Are disclosure problems increasing?

- Are vulnerable client records complete?

- Are annual reviews being delivered?

- Are remedial actions completed on time?

- Are Consumer Duty outcomes being evidenced?

Step 7: Maintain a complete audit trail

A complete audit trail is one of the most important ways to reduce regulatory and operational risk.

It helps firms show:

- What happened

- When it happened

- Who was involved

- What decision was made

- What evidence supported the decision

- What action followed

- Whether the issue was resolved

Where compliance software helps adviser firms reduce risk

Compliance software can help firms move from fragmented, manual processes to a more controlled and auditable way of working.

Compliance risk: manual processes vs compliance software

| Manual spreadsheet-based processes | Compliance software |

|---|---|

| Data stored across separate files | Centralised compliance hub |

| Limited real-time visibility | Live oversight across teams and cases |

| Manual file reviews | Real-time file checking and assisted reviews |

| Weak audit trail | Full process history and user activity tracking |

| Difficult to scale | Designed for growing advice firms and networks |

Why reducing compliance risk is also a business benefit

Compliance is often seen as a defensive function. But good compliance operations can also improve business performance.

- Reduce rework

- Improve adviser consistency

- Speed up case progression

- Support better client outcomes

- Improve management confidence

- Reduce operational bottlenecks

- Prepare for FCA information requests

- Strengthen PI insurance conversations

- Support acquisitions or growth

- Create more reliable management information

A practical compliance risk checklist for adviser offices

Use the following questions to assess whether your current process is helping or hindering your firm:

- Do all advisers follow the same advice process?

- Are file checking standards clearly documented?

- Can you identify high-risk cases before they are submitted?

- Do you have a complete audit trail for each file review?

- Are remedial actions tracked to completion?

- Can managers see live compliance MI?

- Are Consumer Duty outcomes evidenced?

- Can you spot recurring adviser or office-level issues?

- Are templates and checklists version controlled?

- Is compliance activity centralised in one system?

- Are annual reviews tracked effectively?

- Can you respond quickly to a complaint or FCA request?

- Are vulnerable client considerations recorded clearly?

- Do file reviews assess suitability, disclosure and process?

- Is your compliance process scalable as the firm grows?

Final thoughts

Reducing compliance risk in an adviser office is not about adding more administration. It is about creating clearer processes, stronger evidence, better oversight and more consistent file quality.

The most effective firms are moving away from fragmented spreadsheets, manual tracking and reactive file reviews. They are building compliance into the advice workflow, using data to identify risk, tracking actions properly and maintaining a complete audit trail.

For compliance teams, this creates more control. For advisers, it reduces uncertainty and rework. For senior managers, it provides better evidence that the firm is meeting its obligations. And for clients, it supports clearer, more consistent outcomes.

See how BAT supports compliance teams

BAT helps advice firms centralise compliance operations, streamline file checking and maintain a clear audit trail across the business.

Explore Our Compliance Solutions